【摘要】會计英语作为商业信息传递的桥梁,在现代商业中起着重要作用。同时,全球化背景下,越来越多的人学习会计英语,研究会计英语翻译。因此,研究会计英语的特点及其翻译有着重要意义。翻译目的论强调翻译过程中目的的重要性,这符合会计英语翻译的要求。本文将探究会计英语的特点,并结合目的论,研究会计英语的汉译方法,希望对后续的会计英语翻译提供一定借鉴。

【关键词】目的论;会计英语;翻译方法

【作者简介】林清燕,银川能源学院。

I. Introduction

Rapid development of economic globalization has seen deepened opening-up of China and promoted multinational business. Accounting English, a tool to disclose economic statue of companies, plays a part in modern business. And, under globalization, many Chinese study accounting English and its translation, for there is an increasing need to read the financial statements of the transnational corporations. Thus, studying accounting English and its high-quality translation is becoming important. Besides, studying accounting English, English for Special Purpose (ESP), can promote the development of ESP research. Thus, it has both practical and theoretical value. Skopostheory, focuses on purpose of translation, being significant to guide the translation of accounting English. Through the study of Accounting English translation under Skopostheory, the paper is expected to have some significance for the future study.

II. Literature reviewing

The word skopos a Greek word means purpose. Skopostheory was developed in Germany in the late 1970s, put forward by Hans Vermeer raising the skopos to the center of the translation and putting forward three principles in the translation: the principle of purpose, coherence and fidelity. ?Later, the other German translators further developed the theory. At home, Skopostheory, introduced to China in 1980s, has been widely discussed and applied. Gao Wanwei (145-147) combined translation theory with semantic analysis, and discussed translation from two linguistic features and language creation skills. Luo Xiaohong(11-14) analyzed the current research situation and existing problems of translation on Skopostheory. Liu Hong (62-63) discussed language features of accounting English. Song Guanglei (55-56) studied differences between accounting English and general English. Liu Baiyu (63-64) discussed abbreviations and professional vocabulary in accounting English.

After searching related literature, the author finds most studies belong to theoretical study, lacking of practical study to some degree. By studying the translation of accounting English under Skopostheory, this paper attempts to put forward translation methods, hoping to provide some reference for the subsequent translation of accounting English.

III. Introduction to Accounting English

Accounting English differs from general English lexically and syntactically, influencing the choice of translation methods. So, it is necessary to analyze linguistic features of accounting English.

1. Lexical Characteristics

(1) Abundance of Abbreviation

To save space and reduce unnecessary repetition, accounting text has abundance of abbreviation, because it appears in the form of sheets or tables with limited space such as VAT (Value Added Tax) , FIFO(First-in, first-out), PV (Present Value), and Cr. (Credit).

(2) Wide Use of Technical Terms

As a professional language, accounting English has a large number of technical terms. An accounting technical term may be formed by a single noun or by a noun phrase such as “income tax”“profit distribution”“notes receivable”“manufacturing cost”“semi-finished goods”“work in process” and “recoveries of bad debt”.

2. Syntactic Features

Syntax is the analysis of the structure of words in a sentence. Accounting English, a branch of English for special purpose, possesses its unique syntactic features, which may influence translation.

(1)Passive Sentence

In English, passive sentences, preferred in English influenced by western culture, are used often, particularly in professional, technical texts. Using passive sentences in accounting English attempts to make clear and objective description and achieve the effect of being accurate clear and objective.

(2) Complex Sentence

Commonly, there are three kinds of sentences: simple sentences, coordinate sentences and complex sentences. A complex sentence is a sentence with one independent clause and at least one dependent clause. Complex sentences occupy great in accounting English, used to illustrate complicated ideas and making accounting logical, objective and scientific.

3. Rhetoric Features

(1) Seldom Use of Rhetoric Devices

Rhetoric devices, used to persuade readers/listeners or to evoke an emotional response in the audience subjectively, are rarely used in accounting English, including metaphor, irony, alliteration, and simile mainly, because accounting texts carry objective truth and facts. So, using them will destroy the preciseness and strictness of accounting English to some degree.

(2)Poor Choices of Tenses

Tense, category of grammar, indicates time when the situation happens, including present, past, and future mainly. Modern accounting is founded on accrual basis, requiring to record business transaction precisely and immediately, thus making present tense account for a great percentage in accounting English texts.

Ⅳ. Translation of Accounting English under the Guidance of Skopostheory

The primary aim of accounting texts is to pass financial information based on recorded transactions. According to skopostheory, the need of readers, mainly some Chinese in the field of business occupying a great percentage, should be satisfied.

1. Three Criteria of Accounting English Translation

(1) Accuracy

According to skopostheory, accounting English belongs to informative texts, thus whose skopos of translation is to make the target language intact and precisely. Thus, accuracy is very important in accounting English translation. Besides, accounting English featured with technical terms has become a standard language in global business and a false translation can cause misunderstanding and confusion for Chinese readers and even losses of a great fortune.

(2) Brevity

Skopostheory stresses the need of readers. Those people, some Chinese in business field, value time and stress efficiency under which they need to analyze translated information accurately and quickly. Therefore, brevity in translation is necessary. Besides, there are laws, regulations and rules in accounting English written economically, whose nature also decides the concise translation. And, terminologies and abbreviations exist in accounting English. Therefore, translating accounting English should be concise if not causing misunderstanding.

(3) Objective

Accounting, as a carrier of business information, precisely records what happens in daily business without any subjective comments. Due to this nature, accounting materials are written objectively. According to skopostheory, the need of readers needs to be considerated. Thus, being objective is a criterion in accounting English translation.

2. Translation Skills Applied

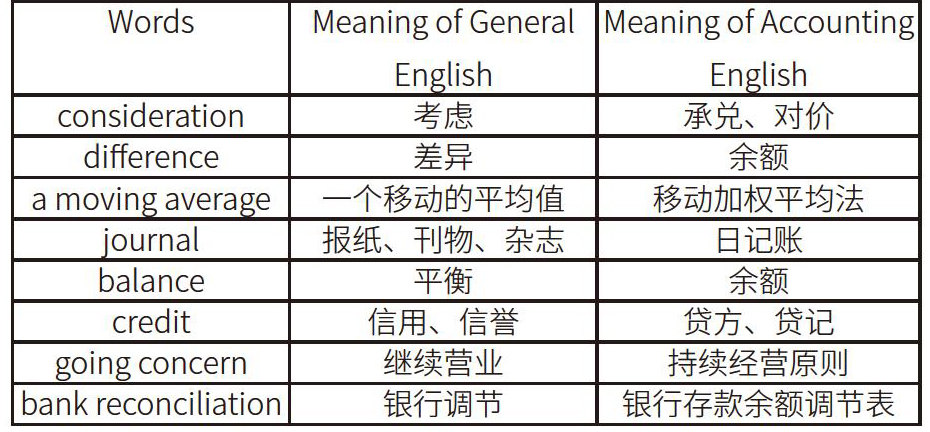

(1) Translation of Technical Words and Phrases

Accounting English are professional English containing a lot of terminologies in accounting records. For translating accounting terminologies, translators need to acknowledge their professional meaning first and then translate them contextually. Some examples are given in the following table:

(2)Translation of Non-technical Words and Phrases

For translating non-technical words and phrases, to fulfill the requirement of Skopostheory, four skills are mainly employed.

Addition is to add new words or phrases in translation, helping target readers to grasp intact meaning of the original. For example,“Essential to the accrual basis is the matching of expenses with the revenue that they helped produce. (權责发生制会计很重要的一点是帮助产生收益的费用与收益相配比).” ?In the example, when translating “essential to the accrual basis”, 一点 has been added to make the meaning more concrete and logic, which is in a line with Chinese idiomatic expression.

Omission is to reduce words and phrases not necessary during translation, thus making the target readers not confused and achieving the criterion of accuracy and brevity. For example, “Accounting is a process of recorded, classifying, summarizing, and interpreting of those business activities that can be in expressed in monetary terms. (会计是一个以货币形式对经济活动进行记录、分类、汇总以及解释的过程).” In this case, “that” is not translated, because translator aims to keep the translation in a line with Chinese grammar.

To meet the need of readers, conversion of parts of speech is used. For example, “Depreciation means the allocation of the cost of a plant asset to expense in the periods in which services are received from the asset. (折旧是指将固定资产的成本分配到该资产提供服务期间的费用中)” In this example, allocation, a noun here, is changed into verb for the sake of Chinese readers.

(3) Translation of Passive Sentences

Passive voice is widely used in accounting English. Generally, translators can keep passive voice unchanged in Chinese texts or change passive voice into active in Chinese, which depends on Chinese grammar or/and Chinese idiomatic expression. For example, “These three basic elements, assets, liabilities and equity, are connected by fundamental relationship called balance-sheet equation, sometimes called simply the accounting equation.(资产、负债和所有者权益三个基本要素由一个叫作资产负债表等式、有时称之为会计等式的关系式联系起来) .” In this case, In this case, passive is changed into active by “由”. Another case is “When an amount is entered on the left side of an account, it is a debit, and the account is said to be debited(当一个数额记在账户的左边,它就是借方记录,这个账户就是被借记) ”. In this case, the passive voice is kept. In short, whether using the passive words or not depends on Chinese idiomatic expression.

(4)Translation of Complex Sentences

In accounting English, there are many complex sentences consisting an independent clause and one or more dependent clauses, which can reflect the logicality and strictness of accounting texts. In view of the systematic and scientific nature of accounting English as well as the need of target readers, the following methods are used commonly: adjustment of word order; conversion of parts of speech; addition and omission.

For example, an account has a debit balance when the sum of its debits exceeds the sum of its credits; it has a credit balance when the sum of creditors is the greater. In double-entry accounting, which is in almost universal use, there are equal debit and credit entries for every transaction. Where there are only two accounts affected, the debit and credit amounts are equal. If more than two accounts are affected, the total of the debit entries must equal the total of the credit entries(當一个账户上借项数超过贷项数时,这个账户就出现了借方余额。但当它的贷项数大于借项数时,就出现了贷方余额。在复式记账法下,每笔交易的借项和贷项记入的数字相等。现在复式记账法在全世界得到了普遍的使用。在只有两个受影响的账户时,借方数额和贷方数额是相等的。但如果涉及两个以上账户时,记入借项的总数必须与记入贷项的总数相等).

In this case, in order to make the translation clear and logic, the translator adjust the order of the first sentence, making the adverbial clause in front of main clause, meeting the need of Chinese reading logic. For the second sentences, “the greater ” is translated as the贷项数大于借项数时,showing addition is used to make the information understandable to the target readers. For the third sentence with attributive clause, the translators divide the complicated sentences into two simple sentences by adjusting the order, making the information expressed in a clearer way. For the fourth sentences, “there be” is omitted to make translation more concise based on the criteria of brevity. For the last sentence, the passive voice is turned into active voice. Besides, debit, an noun here, is translated as 计入结项, a verb. By using conversion of parts of speech, the noun is turned into verb, which makes the translation concise and brief.

V. Conclusion

This paper has introduced the significance of study and the status of domestic and foreign study first. Then, it has analyzed the characteristics of accounting English in a detailed way. Finally, under the Skopostheory, the paper has analyzed translation methods based on three criteria: the criteria of accuracy, the criteria of brevity and the criteria of objectivity. Yet, there is still a lot of research space, and further study will be expected.

References:

[1]Reiss, Katharina & Vermeer, J. Groundwork for a General Theory of Translation[J]. Tubingen: Niemeyer, 1984.

[2]郜萬伟.翻译目的论——松开译者脚下之链[J].河北理工大学学报(社会科学版)社,2007.

[3]刘白玉.会计英语的词汇特征及其翻译策略[J].会计之友2007:63-64.

[4]刘红.成人会计专业英语的语言特点及教学初探[J].北京农业职业学院学报,2004:62-63.

[5]罗小红.翻译目的论之国内研究现状反思[D].新疆建设职业技术学院,2016.

[6]宋光磊.会计英语词汇差异[J].对外经贸财会,2006.

[7]孙坤.会计英语[M].东北:东北财经大学大学出版社,2012.

[8]肖柯欣.会计英语特点及其目的论视角下的汉译[D].天津大学, 2015.

[9]张月娥.文本类型视角下会计英语的语言特点和交际翻译法[D].合肥工业大学,2009.

- 国有企业固定资产的核算问题分析

- 化工企业全面预算管理的困境及对策探讨

- 集团企业司库在资金管理中的运用研究

- 企业发票管理的途径探究

- 精益管理在企业成本管理中的应用

- 加强国有企业内部控制思考

- 浅析日常营运资金预算的优化

- 制造业企业内控管理的关键细节问题分析

- 浅析N商业银行押品管理存在的问题与对策

- 餐饮企业的采购环节内部控制制度研究

- 国有企业资金管理问题及对策

- 企业如何减少“黑天鹅”事件对经营的影响

- 光伏企业预算管理问题及全面预算管理构建

- 浅谈企业价值提升的成本控制路径

- 企业并购重组过程中存在的问题和对策分析

- 浅谈施工阶段的商务管理和控制

- 私募股权投资投后管理现状之我见

- 贸易公司内部控制监督相关问题及应对措施

- 数字化环境下如何提升医院档案管理的有效性

- 事业单位国有资产管理问题思考与优化建议

- 住房公积金流动性风险分析中的计算机仿真

- 事业单位政府采购的现状问题及建议

- 城镇职工医疗保险费用控制的困境与对策

- 城乡居民医疗保险现状分析

- 文化市场中档案行政执法存在的问题与措施

- b-road

- b road

- broad

- broadband

- broad banding

- broadbanding

- broadbands

- broad-bands

- broadbased

- broad-based

- broad-beam

- disgrace¹

- disgracing

- disgress

- disgruntled

- disgruntledly

- disgruntledness

- disguisable

- disguise

- disguise as

- disguised

- disguisedly

- disguisedness

- disguisednesses

- disguiseless

- 杜仲

- 杜伯

- 杜佑

- 杜兰

- 杜勃罗留波夫

- 杜十娘沉百宝箱

- 杜十娘的百宝箱——全部家当

- 杜厥

- 杜口

- 杜口吞声

- 杜口吞声杜口绝舌

- 杜口无言

- 杜口结舌

- 杜口结言

- 杜口绝舌杜口吞舌

- 杜口绝言

- 杜口裹舌

- 杜口裹足

- 杜句驱疟

- 杜嘿

- 杜园

- 杜墙不出

- 杜如晦

- 杜威

- 杜子春